CBOT futures ended slightly lower, but mostly shrugged off weakness in neighboring wheat & soy markets. ARC views strength in corn today as a function of another week of record ethanol production, and the fact that a meaningful pattern shift is still unlikely in Argentina & Southern Brazil by late December.

CBOT futures ended slightly lower, but mostly shrugged off weakness in neighboring wheat & soy markets. ARC views strength in corn today as a function of another week of record ethanol production, and the fact that a meaningful pattern shift is still unlikely in Argentina & Southern Brazil by late December.

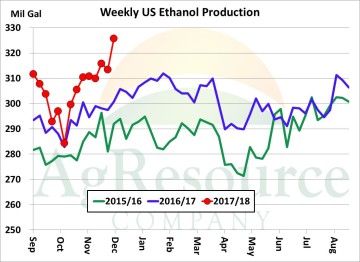

Through the week ending last Friday, US ethanol plants produced a record 326 Mil Gal, a full 10 Mil above the prior record set two weeks ago, and which further argues the USDA’s projected ethanol demand draw is 25-50 Mil Bu too low. Ethanol production margins have eroded rather quickly (calculated today at $.25/Gal, vs. $.60 in early Nov), but ethanol’s discount to gasoline remains substantial, and non-domestic blend disappearance continues at a record pace.

The point is that, fundamentally, we doubt much downside risk exists below $3.45, basis March, and the overall South American weather pattern remains concerning. This is no place to make new sales, and funds may be more willing to part with sizeable short positions by late month if weather doesn’t improve.