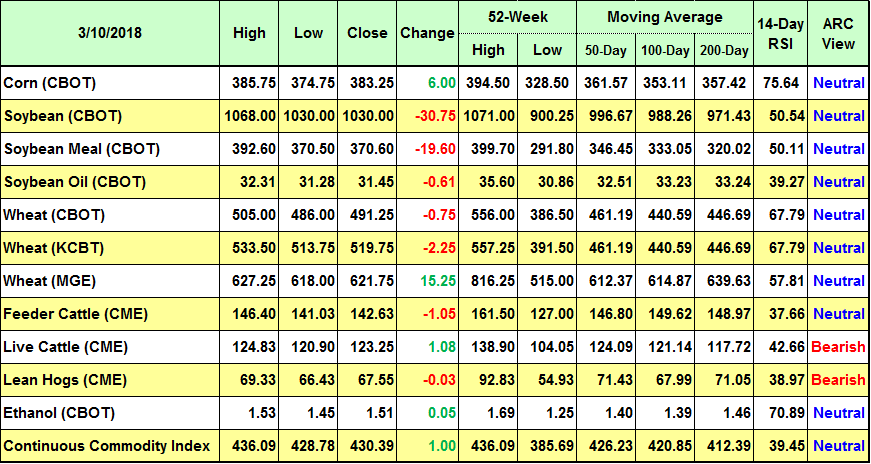

Commodity Index

The CRB Index rallied to fresh ‘18 highs, but resistance against the 2016 high held, and futures softened into the end of the week. A lower close was feared, but energy futures rallied on Friday. So far, it does not appear that the Trump Administration duties on steel/aluminum has had much impact. Traders are waiting for retaliatory measures from China and other key metal exporters before drawing any trading conclusions. The CRB index has been an a general rally phase since May. The next few weeks will be critical in determining whether the uptrend persists? ARC looks for consolidation in coming weeks as the market looks to the value of the US dollar to determine its next move as the Central US Bank raises interest rates. A weaker USD would signal a new rally phase for the CRB

Corn

Corn futures extended their advance with new rally highs. Corn’s story through the middle part of summer is mildly bullish as the US old crop balance sheet tightens and implied new crop stocks rest at a multi-year low. The USDA still has work to do in terms of cutting South American production, and so looks to add more bushels to US export demand. Old crop stocks are likely very close to 2.0 Bil Bu, which assuming steady/lower seedings & trend yield suggest old crop stocks will exist in a range of 1.7-1.8 Bil Bu. This is still a more than adequate, but not long ago, the market was trading old and new crop stocks of 2.4-2.6 Bil. Things have changed enough to support May corn at $3.75-3.80. And until it can be confirmed that US yield is at or above trend, the downside risk is limited. Corn should gain on both wheat and beans over the next several weeks, and we remain patient in extending cash sales – particularly as extreme drought is firmly entrenched across the Plains. Spot corn futures is above a long term downtrend line.

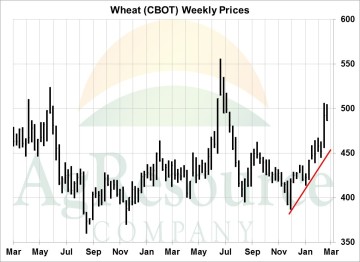

Wheat

Wheat futures were unable to exceed prior week highs, and amid a modestly bearish USDA report, ended the week down 3-10 cents. As expected, the USDA in its Feb report lowered US exports and indeed the market is currently priced well above the rest of the world, limiting export interest from now till June. HRW stocks were raised another 15 Mil Bu to 510 Mil, and since the Nov report have been raised 40 Mil Bu. This will act as a sizable buffer against yield loss in the Plains, and the US all wheat balance sheet looks to be rather comfortable without a Black Sea weather problem this spring – which is not evident as of now. We doubt the market loses its premium entirely, and strong support is offered to May CME at $4.50, but the lack of demand is noteworthy and funds are expected to be more comfortable holding short positions moving forward. ARC maintains a strategy of using rallies to sell 2017, 2018 and 2019 crops. World wheat stocks are still record large.

Soybeans

Soybean and meal markets ended the week lower for the first time since mid January. The March WASDE offered something for both the bulls and the bears, by lowering their estimate for old crop soybean exports/raising old crop stocks, while they also made deep cuts to the Argentine soybean crop and raised US old crop soymeal exports. The initial price response was mixed, while markets fell sharply through Friday’s trade as the 6-10 day EU weather model forecast showed good rains falling across the Argentine soybean belt in late March. With crop maturity already advanced, its not likely that this rain event adds to yield, rather it just stabilizes the crop. But more importantly to the CBOT trade, is that the CoT report showed funds holding a record large bean meal position, and the largest soybean position since July 2016. We expect spot soybeans to find support on a break back to $10, but doubt that a lasting bear market develops amid new crop yield and seeding uncertainty.

Cattle

Cattle futures were back and forth in a wide range, but finished the week with a solid rally on Friday. An early week rally had been stopped by ideas that this week’s cash trade would be lower. April cattle futures fell to a 7 week low. However, the week’s cash business at $126-127 was near steady, and technical buying supported late week trade. Seasonally, cattle and beef prices tend to gain into the spring as domestic demand increases with rising temperatures. However, the bearish supply outlook is unchanged with record large 2nd quarter beef production forecast, following large late 2017 and early 2018 placement totals. Technically, April cattle have held in a wide range from $120-130 since last November, and the very broad range is expected to continue into expiration. It’s summer cattle prices that have the greatest downside risk as demand seasonally slows. A weekly close in April cattle below $121 confirms a downside target of $105 in June or July.

Hogs

April hogs traded on both sides of unchanged through the week before ending firm. The cash hog market scored a major top at $75 in early February and then fell nearly $8 over the course of the following 3 weeks. Cash trade began to stabilize in late February, and held in a very narrow range through this past week. Seasonally, cash hog and pork prices tend to strengthen into the summer as supplies seasonally decline up as domestic demand builds. It’s likely that the market is close to confirming a spring low, but rallies into the summer are expected to be capped in the low $80’s by record large US red meat production. The US March Inventory Report will be released at the end of the month, which is expected to confirm another 1-2% increase in the breeding herd along with another quarter of record large market hog inventories. Our largest market concern is for 4th quarter prices, which are not expected to hold as strong as in 2017.