The world barley market has gotten rather tight amid ever falling planted area, steady consumption, a lack of any real growth in yield, and this year’s drought in Australia. World barley production fell short of consumption in 2016/17, and this year global barley consumption looks to exceed total production by some 5 MMTs. World barley end stocks are forecast by USDA at a record low 18 MMTs, vs. 22 in 2016 and 26 MMTs in 2015, and via cash prices it’s clear the market is running extremely tight on inventory. And like so many other minor feedgrain markets (sorghum, oats, etc.), without expanded seedings in the US and elsewhere in 2018, the world barley balance sheet becomes untenably tight.

The world barley market has gotten rather tight amid ever falling planted area, steady consumption, a lack of any real growth in yield, and this year’s drought in Australia. World barley production fell short of consumption in 2016/17, and this year global barley consumption looks to exceed total production by some 5 MMTs. World barley end stocks are forecast by USDA at a record low 18 MMTs, vs. 22 in 2016 and 26 MMTs in 2015, and via cash prices it’s clear the market is running extremely tight on inventory. And like so many other minor feedgrain markets (sorghum, oats, etc.), without expanded seedings in the US and elsewhere in 2018, the world barley balance sheet becomes untenably tight.

Barley prices are working to secure acres and will continue to do so in the months ahead. As such, our work again suggests corn US & world corn seeding may contract by more than the trade currently anticipates.

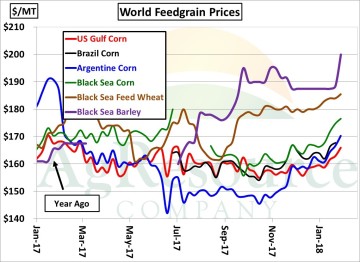

World feedgrain cash prices have changed dramatically in recent months. One year ago, Black Sea barley (the Black Sea accounts for 35-40% of total world barley trade) was the world’s cheapest feedgrain, and even following this year’s harvest Black Sea fob quotes were competitive with other feedgrain offers. However, since summer the Black Sea barley market has rallied some $32/MT (20%), and in just the last week!

World feedgrain cash prices have changed dramatically in recent months. One year ago, Black Sea barley (the Black Sea accounts for 35-40% of total world barley trade) was the world’s cheapest feedgrain, and even following this year’s harvest Black Sea fob quotes were competitive with other feedgrain offers. However, since summer the Black Sea barley market has rallied some $32/MT (20%), and in just the last week!

Black Sea cash offers are up $12/MT to $200/MT or $5.45/Bu. Black Sea barley is now the world’s most expensive feedgrain, and the graphic makes it clear that the rise in S American corn basis, and surging feed wheat and barley prices are working to elevate US corn demand. Black Sea barley acreage will expand at the cost of corn, particularly in Russia.

Price will have to ration available supplies through the balance of the crop year. The table below presents two scenarios for world barley S & D: one in which acres are unchanged, and one in which acres expand enough to keep end stocks/use steady. Assuming mild growth in global barley consumption, our work indicates that 2.2 Mil additional hectares (5.5 Mil acres) are needed to maintain world end stocks of 17 MMTs. Any growth in global barley end stocks requires harvested area closer to 50.5 Mil HA, or expansion of 2.9 Mil HA, which would be the largest since 2013. Until such acreage is confirmed, we expect cash barley prices to move higher, which along with rising feedwheat prices bodes well for global corn trade/demand into September. Global corn acreage, as well as stocks, look to contract in the years ahead which adds another element of support.

Price will have to ration available supplies through the balance of the crop year. The table below presents two scenarios for world barley S & D: one in which acres are unchanged, and one in which acres expand enough to keep end stocks/use steady. Assuming mild growth in global barley consumption, our work indicates that 2.2 Mil additional hectares (5.5 Mil acres) are needed to maintain world end stocks of 17 MMTs. Any growth in global barley end stocks requires harvested area closer to 50.5 Mil HA, or expansion of 2.9 Mil HA, which would be the largest since 2013. Until such acreage is confirmed, we expect cash barley prices to move higher, which along with rising feedwheat prices bodes well for global corn trade/demand into September. Global corn acreage, as well as stocks, look to contract in the years ahead which adds another element of support.